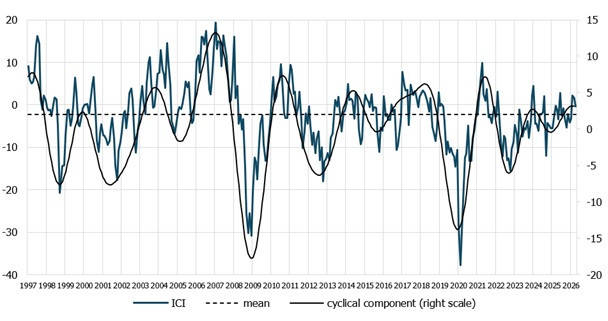

June marked another month of a weakening business climate in the manufacturing sector. The value of the IRG SGH industrial confidence indicator (ICI) fell by 2.0 pts month-over-month. This time, however – unlike a month ago – the decline in the indicator was driven by a fairly significant drop in domestic orders. The ICI currently stands at -0.4 pts, 0.8 pts higher than a year ago. This indicates that the impact of positive cyclical factors is waning – once again, the year-over-year increase in the indicator’s value is smaller than it was a month earlier.

Most of the key balances in the survey responses decreased month-over-month. Only the level of foreign orders increased, and employment rose (slightly, by 1.0 pts). One positive sign is the significant decline (by 17.1 pts, to the level seen in October 2025) in the balance of selling prices for finished goods. Although manufacturers expect prices for their products to rise, the increase is modest, amounting to 3.2 pts. The currently projected price level is close to that prior to the outbreak of the conflict in the Persian Gulf. It is worth noting the sharp decline in the values of the most important indicators of economic activity, namely production volume and orders. The former fell by 9.1 pts, and the latter by as much as 13.6 pts, as mentioned, due to a decline in the volume of domestic orders. The values of both balances remain higher than a year ago, so the decrease in production volume and orders is primarily seasonal in nature. A double-digit (11.2-pt) decline in the balance related to finished goods inventories indicates that demand was largely met by drawing down inventories. Respondents assessed the current situation in the Polish economy as significantly worse than a month ago.

Overall, when comparing the results of the June survey with those from a year ago, it is hard to avoid the impression that the current situation in the manufacturing sector has changed little over the past year. Only production and employment levels are slightly higher. The industry remains stagnant, due in part to the economic downturn across our western border. We continue to observe minor fluctuations in the indicator and the survey’s main balances, which hover around the long-term average (-2.2 pts), showing no upward or downward trend. Survey participants’ forecasts remain optimistic, but the values of the forecast balances offer no hope for a sustained improvement in the business climate in the near future.

Researcher:

Konrad Walczyk, kwalcz1@sgh.waw.pl